(Here is a brief follow-up.)

Long Term Housing, Equity, and Interest Rate Comovement with Demographic Foundations

Here are a couple of articles from the Minneapolis Fed that discuss a series of papers on the similarities of the 2000's and the 1970's, which got me thinking more about aging population and long term macro cycles.

In the 1970s, U.S. asset markets witnessed (i) a 25% dip in the ratio of aggregate household wealth relative to GDP and (ii) negative comovement of house and stock prices that drove a 20% portfolio shift out of equity into real estate.

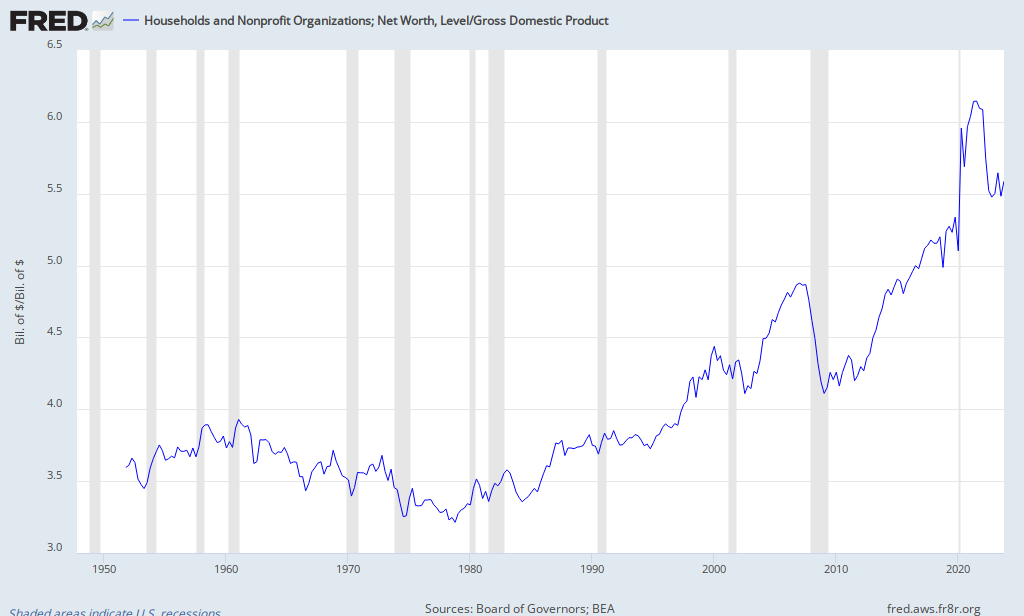

Here is a Fred graph that extends a basic version of their ratio into the 2000's. We can see a similar dip in net worth that comes from a decline in equities in 2000-2002. But in the 2000's, the housing boom was much more extreme, so there is the huge bump in net worth from 2003 to 2007, which breaks down in the financial crisis.

Here is a Fred graph that extends a basic version of their ratio into the 2000's. We can see a similar dip in net worth that comes from a decline in equities in 2000-2002. But in the 2000's, the housing boom was much more extreme, so there is the huge bump in net worth from 2003 to 2007, which breaks down in the financial crisis.Piazzesi and Schneider argue that high inflation was integral in the shift from equities to housing. So, the mystery is, why did we see this effect explode in the 2000's in a low inflation environment?

Here is a graph from P & S, showing Home Price to Rent ratios in a range from 20 to 25, peaking in the 50s, 70s and 2000s (roughly coincident with low real interest rate environments and similar population distributions, with population bulges in late middle age).

Here is a graph from P & S, showing Home Price to Rent ratios in a range from 20 to 25, peaking in the 50s, 70s and 2000s (roughly coincident with low real interest rate environments and similar population distributions, with population bulges in late middle age).In addition, here is an updated Price to Rent graph from Calculatedriskblog that puts the subsequent peak of Home Price to Rents in the mid 30s.

Trying to get at the mystery, I put together a model to find the break-even price of owning a home versus renting, with the following variables:

Expected change in home values

Expected change in rental rates

Real long term risk free rate of interest

Down Payment %

Tax Rate

Home Price, expressed as Price to Rent

I had expected to find large consequences from housing's preferential tax treatment and from low down payments leading to the treatment of home ownership as a call option. I was surprised to find very little effect from these factors. In fact, the benefit of ownership increases with higher down payments. And, in line with P & S, home ownership becomes more profitable with high inflation, ceteris paribus.

So, how could home prices have exploded in the 2000s?

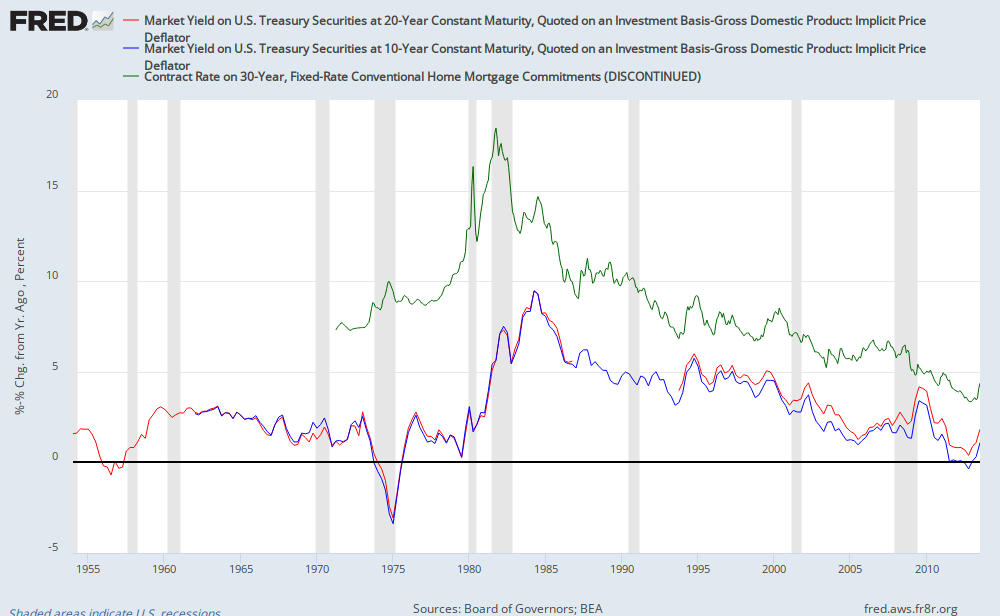

The overwhelming factor justifying a higher Home Price to Rent (PTR) is the real interest rate. That is because much of the value of owning, versus renting, is as a hedge against future nominal increases in rent. And, the present value of those relative gains is very sensitive to real rates. Here is a graph of interest rates:

The green line is the 30 year mortgage rate. The blue and red lines are rough proxies for real 10 and 20 year rates (nominal rates minus the inflation rate). The mortgage spread is pretty stable over time, so most of the difference between the mortgage rate and the real rates is a reflection of the inflation premium.

Using my model, I found that, as an alternative to risk free fixed income, assuming no qualification constraints, the following PTR ratios could be justified simply from changing the level of real rates:

These justified prices assume a reversion to a long term PTR of 24. In other words, the buyer of a house with a PTR of 28.69 can expect the house to lose 17% of it's value in real terms over 30 years, and the 28.69 PTR is still justified.

With naïve price expectations (expected home price growth and expected rent price growth equal to the inflation premium), PTR would range from 17.5 at a 5% real risk free rate to 32.6 at a 1% real risk free rate.

So, we could expect prices very similar to what we saw in the 2000's with little or no bubble behavior.

So why doesn't this show up in the 1970s?

The model justifying the prices of the 2000's has one big assumption - no qualification constraints. No qualification is required on fixed income investments that are alternatives to homes. But, to invest in the home you live in, you have to commit to purchase the entire house. And, the method the bank uses to affirm your investment has nothing to do with a comparison between a long term bond investment and your home. The bank simply compares nominal interest rates to your annual income. So, even though the return on a home investment is higher in a high inflation environment, making nominal payments from your income becomes the constraining factor.

But, even as late as 1979, when mortgage rates were above 10% and rising, PTR was still rising at 25. It was only the advent of higher real rates that sent home prices back down.

Low inflation in the 2000's meant that this constraint was minimal, so the prices that could have been justified in the 1970's in terms of return on investment could now be bid.

How does this change the interpretation of the 2000's?

From this point of view, the home prices of the 2000's were rational. The apparent bubble activity that seems excessive (no doc loans, low down payments, interest only loans, etc.) now can simply be described as methods used to further remove constraints which were keeping investors from making a reasonable real estate investment. Since low inflation caused monthly nominal payments to be low, buyers could reduce capital constraints by using methods that reduced other constraints, such as a down payment, with the cost of increasing the monthly payment. Trends, such as lower down payments, also served to increase the option value of the mortgage, lowering the required return of the real estate. (There might still have been a bubble for AAA rated securitizations at the banks, but if my interpretation of events is plausible, then I don't think the CMO market would have more than a small effect, as long as nominal rates were low enough to reduce the qualification constraint.)

These methods would not have been useful in the 1970's, because the constraint then was in making the monthly payment. A larger, unamortized mortgage principal would have only increased the constraint.

Also, note that before the financial crisis, real rates rose by about 1% from 2005 to 2007. And, coincidentally, PTR peaked in 2005 and fell by about 4 points by the end of 2007. This is exactly the behavior we would expect from a reasonably priced housing market that is constrained by expected returns instead of qualification constraints.

All of those mortgages were basically put options on homes, held short by the banks. And, the Fed caused a deflationary liquidity crisis, starting at the end of 2007, which meant that many of those options were exercised. The image of the Fed as a fat cat stuffing $100's into the tuxedos of its favored friends may be less accurate than the image of a waiter bringing out a free dessert after the chef burnt the entrée.

How does this change our expectations?

We can already see a rebound in the housing market, post-crisis, which is reportedly very heavy in all-cash purchases from sophisticated investors. We don't have an overheated CMO market and we don't even have a generous real estate credit market. What we do have are low real rates and low inflation. I expect that there will be much gnashing of teeth as credit markets loosen up and homeowners take on a larger portion of home purchases as prices rise once again, with stories built around smart money and dumb money. But, it is possible that this will be reasonable behavior. I would expect real rates to rise somewhat as the economy continues to recover, and at some point, as in 1980 and 2006, this will become the constraint for home prices. But, I suspect that we will see PTR at 25 or more before that happens.

And, the really interesting thing to watch will be if the Fed continues to be hawkish on inflation, and real rates fall again within the next decade, while baby boomers are still holding their peak level of low risk savings. It could be possible that even under a conservative regime of mortgage qualification rules, PTR could head well into the 30's again in that environment.

The investment landscape and possible policy reactions, which could be misplaced, in that context, would bear consideration.

This is yet another reason why an inflation rate of 4 or 5% might not be so bad. In addition to preventing sticky wages when inflation in non-cash earnings is high, it would help bond markets clear at rates safely above zero while real rates remain low or negative, and it might just help to stabilize home prices.

That is because much of the value of owning, versus renting, is as a hedge against future nominal increases in rent. Unless you live in the Zoned Zone and want to get on the capital gain roller-coaster.

ReplyDeleteThe US did not have "a" housing boom. The booms were overwhelmingly concentrated in places with constrained housing land supply. Hence the importance of the above factor.

Also, periods of low inflation and high income growth are marked by asset booms (see the C19th). That is because saving is "pushing on" investment, to use Andy Harless's expression. Having supply-constrained housing markets draws such investment to it, to get on the capital-gain roller coaster which is expected to trend continually upwards. Until it doesn't.

Hm. I think we might agree more than you think. Someone in the Zoned Zone would especially need to hedge against nominal increases in rent. There might just be a semantical difference here. More options for building would definitely reduce housing inflation...although, trying to think through it in terms of relative returns to capital in an ultra-low real rate environment, I'm not sure what mechanism would serve to stop the inflow of capital to housing. Would people build larger homes until the values were elevated enough to reduce their relative returns?

DeleteSomeone in the Zoned Zone would especially need to hedge against nominal increases in rent. Nice point. On size of houses, you might want to check Texas, as it was not part of the Zoned Zone and has high population growth, in part because it is not part of the Zoned Zone.

ReplyDeleteRecently, I have commenced a blog the info you give on this site has encouraged and benefited me hugely. Thanks for all of your time & work.

ReplyDeleteTop real estate agents in Manakato MN

Top Real Estate Agents in Brainerd MN