"Very low interest rates drive investors into equities in search of higher yields. This supposedly produces a “wealth effect” whereby the 10 percent of Americans who own about 80 percent of stocks will feel flush enough to spend and invest, causing prosperity to trickle down to the other 90 percent. The fact that the recovery, now in its fifth year, is still limping in spite of quantitative easing is, of course, considered proof of the need for more such medicine."

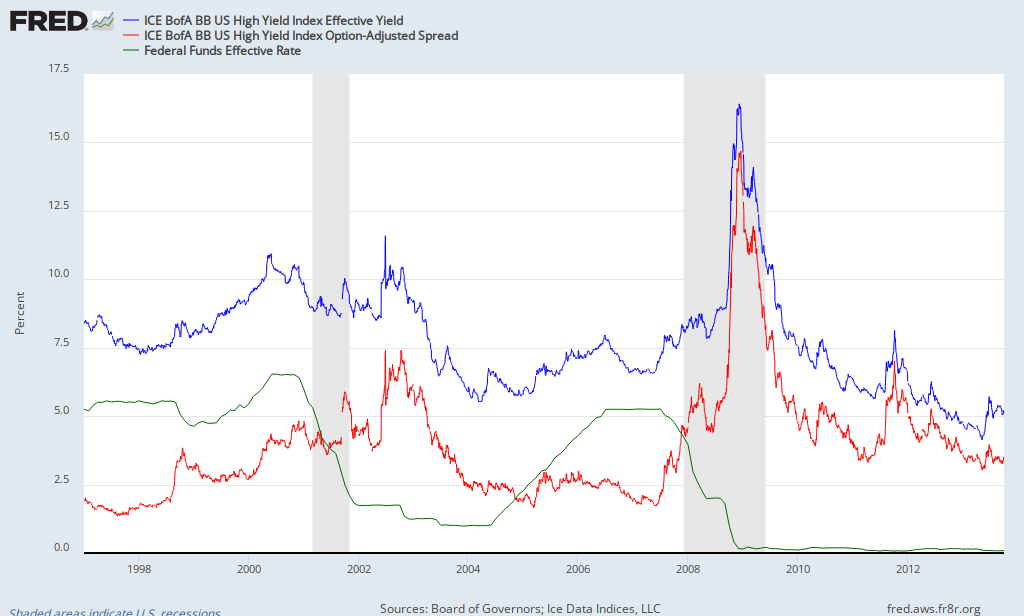

This isn't how it works. Here is a graph of high yield bond rates (blue) high yield spreads (red), and the Fed Funds rate (green). High yield bonds are another supposed area where investors reach for yield, and they correlate highly with equity movements. There is no evidence here of spreads declining when the Fed Funds rate decreases, there is no evidence of spreads increasing when the Fed Funds rate goes up, and there is no evidence that high yield spreads have been especially low since 2010, while the Fed Funds rate has been near zero and the Fed is supposedly flooding the markets with money.

This isn't how it works. Here is a graph of high yield bond rates (blue) high yield spreads (red), and the Fed Funds rate (green). High yield bonds are another supposed area where investors reach for yield, and they correlate highly with equity movements. There is no evidence here of spreads declining when the Fed Funds rate decreases, there is no evidence of spreads increasing when the Fed Funds rate goes up, and there is no evidence that high yield spreads have been especially low since 2010, while the Fed Funds rate has been near zero and the Fed is supposedly flooding the markets with money. Here is a graph of the period since Fed Funds hit zero, where I have replaced the Fed Funds rate with excess reserves as a signal of Fed easing. I presume that everyone agrees that accommodation was ok when spreads were above 10%. In late 2010, when QE2 was implemented (the rise in the orange line), high yield bond rates held fairly steady. Spreads (the red line) did fall, but they fell while risk free rates were rising (the green line - 5 year treasuries). When QE2 was stopped, risk free rates plummeted and spreads shot up. We see a similar dynamic during QE3. Here, high yield spreads are fairly stable and high yield rates are being driven up by rising risk free rates.

Here is a graph of the period since Fed Funds hit zero, where I have replaced the Fed Funds rate with excess reserves as a signal of Fed easing. I presume that everyone agrees that accommodation was ok when spreads were above 10%. In late 2010, when QE2 was implemented (the rise in the orange line), high yield bond rates held fairly steady. Spreads (the red line) did fall, but they fell while risk free rates were rising (the green line - 5 year treasuries). When QE2 was stopped, risk free rates plummeted and spreads shot up. We see a similar dynamic during QE3. Here, high yield spreads are fairly stable and high yield rates are being driven up by rising risk free rates. Let's look at stocks. Here is the relationship between stock prices and the Fed's balance sheet since 2008. This is the supposed smoking gun for conventional wisdom.

Let's look at stocks. Here is the relationship between stock prices and the Fed's balance sheet since 2008. This is the supposed smoking gun for conventional wisdom. |

| Oops - changes at Fred since this was posted have broken this graph. |

In the 1970's, inflation fluctuated between 6% and 14%. Equities showed no gains between1973 and 1982, even though inflation was excessive. These are nominal equity values, so in real terms, equities were seeing huge losses. It was only after the Fed Funds rate was held at very high real levels and inflation dropped below 5% that equities entered the long term bull market of the 1980's and 1990's.

The reason that Fed accommodation has recently coincided with bullish economic experience and very low inflation is because it's the right policy to have, and because the economy is desperate for loose policy. If equities rise due to loose money, then why didn't they skyrocket in the 1970's?

Further, there is nothing "trickle down" about this. The rise in the stock market, as I have shown above, has nothing to do with decreasing yields pushing money into Wall Street. And, since when are tight credit markets good for the middle class?

"Easing serves two Obama goals."

First, Obama appears to buy into the same anti-empirical daydream that George Will does. There is no evidence that he is particularly intent on easing. He frequently repeats the same worries about phantom Fed-created bubbles. He frequently leaves Fed seats open for long periods of time. Despite his lack of attention, the FOMC is mostly peopled by his appointees at this point, and the FOMC seems to represent his lack of a coherent vision for monetary action. This inflation rate is hardly the result of a President bent on devaluing the dollar. Compare this to the earlier chart of inflation in the 1970's.

First, Obama appears to buy into the same anti-empirical daydream that George Will does. There is no evidence that he is particularly intent on easing. He frequently repeats the same worries about phantom Fed-created bubbles. He frequently leaves Fed seats open for long periods of time. Despite his lack of attention, the FOMC is mostly peopled by his appointees at this point, and the FOMC seems to represent his lack of a coherent vision for monetary action. This inflation rate is hardly the result of a President bent on devaluing the dollar. Compare this to the earlier chart of inflation in the 1970's."It enables the growth of government by deferring its costs with cheap borrowing."It would be pretty hard for easing to enable government to defer its costs with cheap borrowing, since Treasury rates have shot up with each round of QE.

"And it redistributes wealth: By punishing savers, it effectively transfers wealth from them to borrowers."Do you know what's another word for "savers"? "Wall Street". It's amazing how a synonym can change your feelings about something. So, within 2 paragraphs, Will has averred that monetary easing both creates a "wealth effect" for asset owners and also punishes savers. The mechanism he claims QE works through is lower rates, which, if true, would actually help existing savers who own fixed rate bonds. He is worried about creating inflation, which would help debtors and homeowners. And, in any case, the QE's have neither produced lower rates nor excessive inflation. This is like towing a trailer backwards, down the wrong lane of a freeway, in reverse. There are so many things wrong here, it is hard to know which way is which. But, the crazy thing is, Will is the one with the conventional take on this issue. The whole country seems like they are towing their trailers backwards down the wrong side of the freeway in reverse.

He then proceeds to compare Janet Yellen's coming relationship with the Senate Banking Committee to Arthur Burn's relationship with Richard Nixon. I suppose Nixon serves as a reminder that apathy is hardly the worst trait we could ask for in a president. As suboptimal as it is, apathy about monetary policy might be the best policy we could hope for from President Obama. When he briefly decided to care about it, he was pushing for Larry Summers, who was ready to slay all George Will's phantom monetary demons.

PS. This is an interesting question about markets, too. When markets insist on performing in opposition to continued consensus expectations to the contrary, is it because Wall Street is full of fund managers secretly investing against the op-eds of the nation's newspapers? Or, are markets finding the right prices even though the conscious consensus of the traders themselves is wrong? I suspect Hayek's "Use of Knowledge in Society" is in high gear. And, I suppose there is always the possibility that I am wrong.

George Will understands monetary policy every bit as well as Barack Obama understands insurance. And they're both equally confident in their ability.

ReplyDelete+1

Delete