Here are some charts of housing starts, which include manufactured housing, which I think brings up an interesting point about perceptions during the housing boom.

The first graph is of homes built for sale and homes built by owner. Note that there was a sharp uptick in homes built for sale, but homes built by owner had actually fallen.

The first graph is of homes built for sale and homes built by owner. Note that there was a sharp uptick in homes built for sale, but homes built by owner had actually fallen. The next graph has the total level of 1 unit housing starts, plus multi-unit starts, plus manufactured home shipments, and the total starts and shipments of all types. They each include a dotted line of the average level over the period of the data in the chart. I haven't taken the time to do it here, but if we just use the average for 1963 to 2005, before the bust, total starts and shipments was barely even above the average. We can see here that, even without adjusting for population, housing starts + shipments at the peak in 2005 were normal for an expansionary period.

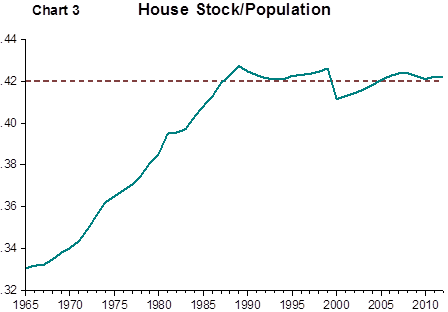

The next graph has the total level of 1 unit housing starts, plus multi-unit starts, plus manufactured home shipments, and the total starts and shipments of all types. They each include a dotted line of the average level over the period of the data in the chart. I haven't taken the time to do it here, but if we just use the average for 1963 to 2005, before the bust, total starts and shipments was barely even above the average. We can see here that, even without adjusting for population, housing starts + shipments at the peak in 2005 were normal for an expansionary period. That is why the housing stock, relative to the population was flat. (It was actually declining relative to the population over 16 years of age.) There wasn't even a housing boom. We all just decided to freak out about the one type of homebuilding that was growing - single family units for sale - and ignore every single other category of housing supply, which included homes built by owner, multi-unit homes, and manufactured homes. All of those categories had been in decline. Of course, it was the decline that created the illusion of a boom, because it was precisely those cities where we can't build, yet where income opportunities are available, where home prices were skyrocketing, because households were bidding up the stagnant pool of homes in those cities in an attempt at economic opportunity in a country that has become inflexible.

That is why the housing stock, relative to the population was flat. (It was actually declining relative to the population over 16 years of age.) There wasn't even a housing boom. We all just decided to freak out about the one type of homebuilding that was growing - single family units for sale - and ignore every single other category of housing supply, which included homes built by owner, multi-unit homes, and manufactured homes. All of those categories had been in decline. Of course, it was the decline that created the illusion of a boom, because it was precisely those cities where we can't build, yet where income opportunities are available, where home prices were skyrocketing, because households were bidding up the stagnant pool of homes in those cities in an attempt at economic opportunity in a country that has become inflexible.In an economy that has arbitrary limitations on supply, especially political limitations, the least powerful citizens get pushed aside. They have been getting pushed aside - pushed from New York and Boston and California to Atlanta and Dallas and Phoenix and Riverside. Now they can't even be pushed, because we decided only the wealthiest can get mortgages. We need to protect the others. So now they are nice and safe between a rock and a hard place. It is true. If we prevent them from ever owning anything, we will be preventing them from ever having a default or a foreclosure. That's how much we care.

You know all these discussions serious people have been having for a decade about the housing bubble and the oversupply that inevitably had to pop? We didn't even have it. Didn't exist. Never happened. We might as well be arguing about what caused the sudden rise of civility in American politics.

Here is a map of shipments by state. Guess which states tend to accept a lot of shipments of manufactured homes, which are an inexpensive way for low income households to become homeowners.

Love the manufactured homes. I guess they don't handle cold weather. Or maybe cheap housing up north anyway. Not sure if the US should promote homeowners but should build tons of housing. No more zoning!

ReplyDeleteThe mobile home distinction is part of the problem. They can easily be placed on a permanent footing and are no longer mobile. That would give us a huge amount of affordable housing that many people would be more than happy living in. These are not your parents/grandparents 1970's crappy single wides. these are 2500+ sqft beautiful homes.

ReplyDelete