I think, on this topic, it is important to distinguish between real (making stuff) and nominal (exchanging money for stuff) economic activity. This is purely a nominal issue. So, I think instead of framing this as an issue of households overconsuming in an unsustainable way, it is more accurate to say that, of the stuff we were making, real estate beneficiaries were claiming more of it, at the expense of people who were producing stuff. That should be inflationary. And, if it is not, then it means that the central bank is counteracting the phenomenon with tight money.

Whatever the inflation effect, real estate owners were consuming, in the real sense, at the expense of producers.

The research referenced in the article also mentions that real estate gains draw some owners out of the labor force because of their newfound wealth. This makes sense. But, again, thinking about this in terms of real economic claims on production, we might expect a similar rise in labor force participation among producers whose incomes are now vying for a smaller portion of production.

|

| Source |

This makes sense to me, because I don't think credit supply or irrational speculation have much to do with the housing "bubble". I think it mostly had to do with high skilled working people buying access into the Closed Access labor markets where limited housing serves as a gatekeeper. So, there while there was certainly some amount of typical labor force reductions because of capital gains, many of the households utilizing gains from those homes for consumption were in those homes specifically to work.

In any case, I don't see much cause for even bringing the central bank into this. From the point of view of consumers who don't have access to these capital gains, this seems like a real shock. There is less production for them to claim. That is going to be the case regardless of the inflation rate. Monetary policy can't solve the problem of unsustainable consumption, even if that is what is happening.

But, households can't unsustainably consume, domestically. They can only change their relative claims on existing production. Here, the trade deficit seems to suggest unsustainability. In effect, foreign capital was flooding into our capital markets, helping to push up home prices, so that, in effect, we were borrowing from foreigners in order to buy production from foreigners, and this is why it was unsustainable.

And, this is why a clear understanding of what has been happening in foreign trade and investment is key. It is true that the trade deficit ballooned during the housing "bubble" as foreign investment flooded into the US. But, at the same time, US net income on foreign investment was also strong and positive. If we were hawking our futures for unsustainable consumption, then our net foreign income should have dropped as foreign savers claimed their profits from our borrowing. Considering the significant spike in net imports, this should be a shocking piece of evidence.

|

| Source |

Yet, again, whether this consumption was sustainable or not, what does the central bank have to do with it? That will be the case regardless of the rate of inflation. The only way for monetary policy to cut into this consumption is to create a real shock large enough to induce retrenchment. This is basically what we did.

|

| Source |

For the period from 2001 to 2006, this growth in mortgage credit accounts for the entire growth in PCE. Might it have been the case that homeowners with windfall gains were claiming all of the marginal new consumption since 2001? Could it be that producers (workers and investors) didn't increase their consumption at all - even in nominal terms - during the housing boom? Could it be that they were working harder just so they could produce more for the housing windfall spenders?*

Mian & Sufi do estimate that 2.8% of GDP was funded by home equity borrowing every year from 2002 to 2006. That's enough to cover the growth in personal consumption expenditures shown above.

Again, short of causing a real shock to incomes, I'm not sure what monetary policy could do about this. A rise or drop in inflation would have presumably increased or decreased nominal spending from both the windfall spenders and producers.

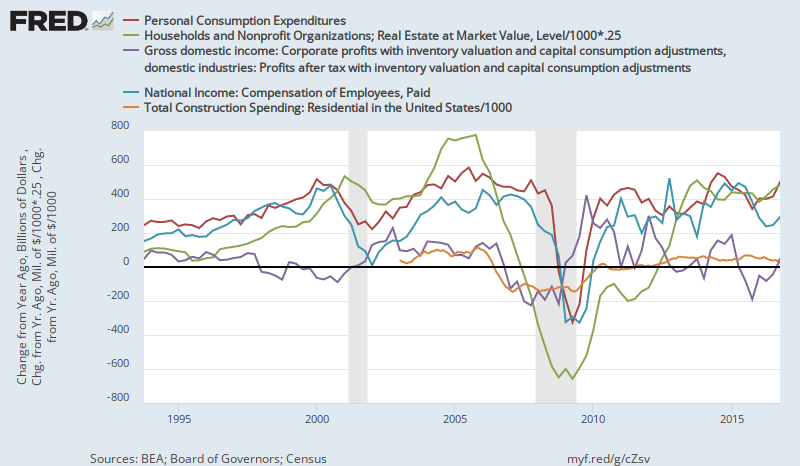

As we can see in the graph, real estate values were the first thing to stop expanding. We might expect some stickiness in the willingness of households to continue tapping home equity for consumption. So, mortgage expansion continued until early 2008. And, PCE growth continued to expand along with mortgage growth. So, for most of 2006 and 2007, marginal new consumption was still being claimed by homeowners, but now it was coming at the expense of home equity.

But, as I have documented, at this point, much of this equity harvesting wasn't from continuing homeowners. There was a spike of selling out of homeownership. The homeownership rate was declining, even though the natural inflow of first time buyers tends to be fairly stable. This meant that housing starts were collapsing and the typical owner of the housing stock was becoming more leveraged, just because long time owners were being replaced by new owners. We can see this where total growth in gross mortgages outstanding was dropping much faster than mortgages outstanding net of new investment.

This is because much of that mortgage growth and consumption growth was funding savings. The way it was funding savings was that first time homebuyers were buying homes from long term homeowners who were exiting homeownership. This created significant new mortgage debt. But, the former home equity of those former home owners wasn't being consumed. It was being saved. Much of it was funding CDOs. This didn't show up as savings, because we don't tend to count capital gains as savings. But, there was a lot of savings flowing out of home equity and into fixed income securities.

Notice that compensation and PCE dropped together in 2008 about when mortgage growth dropped. Mortgage growth dropped after the private securitization market collapsed in summer 2007. At that point, a financial crisis had begun to build, and the Fed was making emergency loans to troubled financial firms. From summer 2007 until they were running out of treasuries to sell in September 2008, they were "sterilizing" those loans. In other words, they were trying to save banks without actually injecting cash into the economy.

But, if consumption was being facilitated by real estate gains and expanding mortgages, then really, from 2004 to 2007, the Fed had already been sort of sterilizing the money supply, sucking out currency to make up for the extra consumption that was funded by real estate gains. When the private securitization market collapsed, if estimates of homeowner debt utilization are accurate, then when the Fed was sterilizing their emergency loans in order to avoid providing money to the economy, they should have been shoveling massive amounts of cash into the economy to make up for the drop in nominal spending.

It isn't the Fed's job to impose a negative shock to make up for past consumption. It's the Fed's job to provide stability. In fact, I submit that the Fed should have been providing more accommodation back in 2006 when home equity started to dive. This sharp increase in homeowner leverage was already a sign of dislocation. We can see in the graph above that, while compensation didn't suffer much from that dislocation, domestic corporate profits did. And, we can see the drop in domestic corporate profits was largely due to the collapse in residential investment.

|

| Source |

So what kept us afloat between 2006-2008? Those foreign profits. Here is a chart of US corporate foreign profits as a percentage of GDP.

________________

* This transfer of consumption is accounted for, to a certain extent by the high incomes of Closed Access producers. The high incomes of Closed Access workers and firms mean that production from Closed Access industries is more expensive - there is less consumer surplus from those industries. So, some of the reduced real consumption is from producers in the rest of the country, who pay more for Closed Access output. Some of the reduced real consumption is from producers in the Closed Access cities who pay more for housing, leaving less of their incomes for other consumption.

I think this paper agrees with you in part, though it is a bit dated.

ReplyDeletehttp://www.bis.org/publ/work223.htm

I sometimes wonder if it is "easier to make money" overseas.

The US economy is very competitive, and foreign firms do not make much profit here, but US firms overseas do make money, especially when they introduce first-world operations to emerging nations, or US efficiency to Europe.

Maybe profits are reported offshore to avoid US taxes.

Also, there was a round of foreign buying of US assets in the 1980s through the early 2000s that did not pan out. Japanese were big buyers of West Coast real estate in the 1980s and 1990s that mostly crapped out. Somebody in Europe bought Chrysler and lost $10 bil.

Still not sure how this plays into your real estate closed-cities explanation.

Evidently, the US has had very profitable overseas operations going since well before 2007 (date of paper).

Also, the NY Fed found many nations---not just the U.S.---running large trade deficits had the house-price booms. The same explanation applies to all such nations?

https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr541.pdf

Basically, the money that bought imported goods and services came back as real estate investments, whether the US, Australia or Spain. This makes sense to me.

To further confuse matters, I have always been a bit suspicious of the international trade stats. Huge amounts of cash, digital and paper, sloshing around in offshore, in Cayman Island-land.

Maybe $30 trillion in the offshore financial netherworld, and growing.

$1.5 trillion in paper US cash is in circulation, or $4,700 for every resident of the country, including babies and old ladies.

Really? If this paper cash turns over even three times a year, it is large relative to reported size of US economy.

Non-PC question: If you had to just tax only imports or on;y labor, which would you tax?

PS Your last chart---why is that only foreign profits? Am I missing something?

Well, great post. Maybe this one is over my pay grade.

Thanks for the link.

DeleteI think the international correlation bolsters my point. Yes, the same thing is happening everywhere. I like this line of thinking. I think I might incorporate this approach in the book. Basically just start with a single fact, which is well established - closed access home values are due to persistent increases in local incomes and rents that are made possible by limited supply. Just follow the logic from there. You get lower interest rates, higher labor participation, trade deficits, mortgage growth, etc. It matches the data better than the demand side explanation or the foreign saver explanation.

I don't understand your last question. On the question of taxes, simply considering the implications of this issue and nothing else, I might favor the import tax. The reason is that my understanding from seeing the discussion about the proposed border tax is that the import tax would actually end up taxing the excess foreign profits of the Closed Access firms. That's probably bad for US incomes in the short term, but I'd prefer not to have incomes based on political exclusion.

Delete"[R]eal estate owners were consuming, in the real sense, at the expense of producers." How "at the expense of"? The real estate owner who finds that his house has appreciated offers a new saving opportunity to someone else: lend me some money, against my house as collateral, and I will pay you interest at an attractive rate. This other person (in practice there will usually be a bank or the like as intermediary) curtails consumption he otherwise would have engaged in and instead lends money at interest to the homeowner. The lender's hypothetical consumption is replaced by the homeowner's consumption, but the lender is gaining interest payments that (over-)compensate him for his foregone consumption. What happens might be said to be "at the expense of" the lender's *consumption*, but not at the expense of *the lender*.

ReplyDeleteWhat if the homeowner normally save $20,000 of his income, but since his home appreciates an extra $20,000, he consumes $20,000 instead? This would have an inflationary effect on consumption goods and would induce some marginal additional savings from other consumers.

DeleteWhat is it that is different about our scenarios that produces different outcomes?

Interest rates will rise because the homeowner (rather than borrowing from someone else) has reduced his own lending. Other people will consume less and save more, getting higher interest on those savings. Why think they will be worse off as a result--why think that the homeowner's gain is "at the expense of" anyone else? (Of course, we are both making a lot of background assumptions, without which we would simply be "reasoning from a price change.")

DeleteThere is a lot going on. I'm admittedly still working it out. Thanks for the input. I'll have to think on it.

Delete"So what kept us afloat between 2006-2008? Those foreign profits. Here is a chart of US corporate foreign profits as a percentage of GDP."--Kevin Erdmann

ReplyDeleteThe chart closest to the above sentence seems to be a start about domestic corporate profits, with some adjustments. Not sure I understand the drift.

Maybe there is a better way to get at it. What I tried to do is take total US corporate profits and subtract domestic profits, which would leave foreign profits.

DeleteKevin, Losses on MBS. RMBS or CMBS. How does that show up in the trade stats? I'm thinking about US imports a widget, foreigner uses money to buy an MBS. That adds to our trade deficit (and current account deficit) at that time, and adds to our capital account surplus at that time. But then there is a loss on the MBS (mortgage defaults, foreclosure, etc., so a permanent loss, not just a price change during the holding period). Where does that loss get shown in our accounts? Thanks!

ReplyDeleteEven for firms, this would show up in Financials in a number of different ways, depending on how each security was accounted for. But I would expect that this lowered the value of foreign owned assets and lowered their income temporarily. I would guess that in the broad scheme of things, that doesn't amount to that much though. Probably more losses came through home equity declines on owned real estate.

Delete